Frequently asked questions

When it comes to making a financial decision, it's important to ask questions. Here are the answers to some of your most common ones.

For Account Owners

Read our how-tosMost common ScholarShare 529 questions

With your ScholarShare 529, you're never locked in. You'll always have access to several options for this money:

- Your funds can be used to pay for a variety of eligible education expenses, including at any accredited college, university, apprenticeships, community college or postgraduate program in the United States—and even some schools abroad.1

- Your 529 can be used for student loan repayment up to a $10,000 lifetime limit per individual.1

- Your funds can be used to pay for K-12 qualified expenses - up to $20,000 annually can be used per student at a public, private, or religious elementary, middle, or high school. Qualified education expenses include curriculum, instructional materials, tutoring by approved professionals, standardized test and dual enrollment fees, and licensed educational therapies for students with disabilities. Click here for more information on recent changes to qualified expenses.2

- You can transfer the funds to another eligible beneficiary, such as another child, a grandchild, yourself or a friend.

- If you just want the money back, you can withdraw the funds at any time. If funds are withdrawn for a purpose other than qualified higher education expenses, the earnings portion of the withdrawal is subject to federal and state taxes plus a 10% additional federal tax on earnings (known as the "Additional Tax"). Non-qualified withdrawals may also be subject to an additional 2.5% California tax on earnings. See the Plan Description for more information and exceptions.

- Or you can always wait because the funds never expire, and often the choice to go to school is a delayed decision. So if your child changes their mind down the road, your savings will still be available.

- Pay for qualified expenses when enrolled in a recognized postsecondary credentialing program. Click here for more information on the recent changes to qualified expenses.3

Footnotes

- 1Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances. Read about eligible education expenses.

Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩ - 2Withdrawals for K-12 qualified expenses can be withdrawn free from federal tax. For California taxpayers, any earnings portion of these withdrawals are subject to state income tax and an additional 2.5% California tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

- 3Withdrawals for Recognized Postsecondary Credentialing Programs—including tuition, books, equipment, supplies for the enrollment or attendance, testing fees if required to obtain or maintain a Recognized Postsecondary Credential, fees for continuing education if required to maintain an Recognized Postsecondary Credentialing Program and therapies for students with disabilities—are exempt from federal income tax. Consult a tax professional for guidance.↩

Your contributions will always be yours, and you do not need to be a resident of California to open, contribute to or use a ScholarShare 529. Your ScholarShare 529 can also be used for a range of qualified expenses in state, out of state and abroad. If you move to another state, you can keep your money invested and continue making contributions to your ScholarShare 529 account—no problem!

There's no cost associated with opening a ScholarShare 529 account or owning more than one account. You could open a different account for each child.

You might do this to align investment strategies with the time frame each child will begin using the funds. For example, an older child's account could be more conservatively invested to help protect your contributions as they near college, whereas a younger child's account might be invested to balance growth and income strategies during a longer time frame. You may also prefer to pay college expenses first out of your highest growth account to maximize federal tax benefits and to encourage gift contributions from friends and family.

Keep in mind: ScholarShare 529 allows you the flexibility to select multiple investment portfolios within each account. This offers you more control to manage risk on your terms. For example, adding the Guaranteed Portfolio Option can help ensure a portion of your college savings is principal-protected.

Multiple accounts can also aid in estate planning by ensuring that college funds are allocated appropriately to each beneficiary upon the death of the account owner. But if you'd like to stick to one account, you can change any eligible beneficiary at any time and at no additional cost.

There is no federal income tax deduction for 529 plan contributions, regardless of where you live, or which 529 plan you participate in.

No. Your ScholarShare 529 funds can be used at any accredited university in the country—and even some abroad. This includes public and private colleges and universities, apprenticeships, community colleges, graduate schools and professional schools.1 Up to $20,000 annually can be used toward K-12 qualified expenses.2 In addition, your 529 can be used for student loan repayment up to a $10,000 lifetime limit per individual.1 Review a list of qualifying expenses and the state tax treatment of withdrawals for these expenses in the Plan Description.

Footnotes

- 1Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances. Read about eligible education expenses. Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩

- 2Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school can be withdrawn free from federal tax. For California taxpayers these withdrawals are subject to state income tax and an additional 2.5% California tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

Qualified higher education expenses include tuition, certain room and board expenses, fees, books, supplies and equipment required for the enrollment and attendance of the beneficiary at an eligible educational institution. This includes most postsecondary institutions. When used primarily by the beneficiary enrolled at an eligible educational institution, computers and related technology such as internet access fees, software or printers are also considered qualified higher education expenses.

Qualified higher education expenses also include certain additional enrollment and attendance costs at eligible educational institutions for any beneficiary with special needs.

Qualified higher education expenses also include (a) qualified expenses in connection with enrollment or attendance at a K-12 primary or secondary public, private or religious school (up to a maximum of $20,000 of distributions per taxable year per beneficiary from all Section 529 programs)1; (b) expenses for fees, books, supplies and equipment required for the participation of a beneficiary in a certified apprenticeship program2; and (c) qualified expenses related to enrollment in a recognized postsecondary credentialing program; and, amounts paid as principal or interest on any qualified education loan of either the beneficiary or a sibling of the beneficiary (up to a lifetime limit of $10,000 per individual).2 (d) make student loan payments. Review the Plan Description for additional information, including the state tax treatment of withdrawals for these expenses.

Footnotes

- 1Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school can be withdrawn free from federal tax. For California taxpayers these withdrawals are subject to state income tax and an additional 2.5% California tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

- 2Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.

Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩

For Account Owners

Read our how-tosAll Frequently Asked Questions

About 529 plans

A 529 plan is a tax-advantaged savings plan designed to help families save for college and a range of other qualified education expenses. 529 refers to Section 529 of the Internal Revenue Code. Read more here: Benefits of a 529

ScholarShare 529 provides a unique set of benefits that can mean more flexibility and growth potential, including:

- Tax-free qualified withdrawals

- Low fees and expenses

- Smart and easy to choose investment options

- Favorable financial aid treatment

- Use for a wide range of education expenses and programs—in California and around the world

Get more details and compare savings options.

With your ScholarShare 529, you're never locked in. You'll always have access to several options for this money:

- Your funds can be used to pay for a variety of eligible education expenses, including at any accredited college, university, apprenticeships, community college or postgraduate program in the United States—and even some schools abroad.1

- Your 529 can be used for student loan repayment up to a $10,000 lifetime limit per individual.1

- Your funds can be used to pay for K-12 qualified expenses - up to $20,000 annually can be used per student at a public, private, or religious elementary, middle, or high school. Qualified education expenses include curriculum, instructional materials, tutoring by approved professionals, standardized test and dual enrollment fees, and licensed educational therapies for students with disabilities. Click here for more information on recent changes to qualified expenses.2

- You can transfer the funds to another eligible beneficiary, such as another child, a grandchild, yourself or a friend.

- If you just want the money back, you can withdraw the funds at any time. If funds are withdrawn for a purpose other than qualified higher education expenses, the earnings portion of the withdrawal is subject to federal and state taxes plus a 10% additional federal tax on earnings (known as the "Additional Tax"). Non-qualified withdrawals may also be subject to an additional 2.5% California tax on earnings. See the Plan Description for more information and exceptions.

- Or you can always wait because the funds never expire, and often the choice to go to school is a delayed decision. So if your child changes their mind down the road, your savings will still be available.

- Pay for qualified expenses when enrolled in a recognized postsecondary credentialing program. Click here for more information on the recent changes to qualified expenses.3

Footnotes

- 1Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances. Read about eligible education expenses.

Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩ - 2Withdrawals for K-12 qualified expenses can be withdrawn free from federal tax. For California taxpayers, any earnings portion of these withdrawals are subject to state income tax and an additional 2.5% California tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

- 3Withdrawals for Recognized Postsecondary Credentialing Programs—including tuition, books, equipment, supplies for the enrollment or attendance, testing fees if required to obtain or maintain a Recognized Postsecondary Credential, fees for continuing education if required to maintain an Recognized Postsecondary Credentialing Program and therapies for students with disabilities—are exempt from federal income tax. Consult a tax professional for guidance.↩

Your contributions will always be yours, and you do not need to be a resident of California to open, contribute to or use a ScholarShare 529. Your ScholarShare 529 can also be used for a range of qualified expenses in state, out of state and abroad. If you move to another state, you can keep your money invested and continue making contributions to your ScholarShare 529 account—no problem!

No. Your ScholarShare 529 funds can be used at any accredited university in the country—and even some abroad. This includes public and private colleges and universities, apprenticeships, community colleges, graduate schools and professional schools.1 Up to $20,000 annually can be used toward K-12 qualified expenses.2 In addition, your 529 can be used for student loan repayment up to a $10,000 lifetime limit per individual.1 Review a list of qualifying expenses and the state tax treatment of withdrawals for these expenses in the Plan Description.

Footnotes

- 1Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances. Read about eligible education expenses. Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩

- 2Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school can be withdrawn free from federal tax. For California taxpayers these withdrawals are subject to state income tax and an additional 2.5% California tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

529 plans can vary in a number of ways. ScholarShare 529 offers a variety of benefits including:

- Tax-free qualified withdrawals

- Low fees

- Funds may be used for all eligible expenses

- Family and friends can gift

- Open an account with any amount

Tax considerations for a ScholarShare 529 account

ScholarShare 529 provides the maximum allowable 529 plan tax benefits available to California taxpayers. When you contribute to a ScholarShare 529, any account earnings can grow federal and California income tax-deferred until withdrawn. In addition, withdrawals used to pay for qualified education expenses are free from federal and California income tax.

There is no California state income tax deduction for contributions made to ScholarShare 529 or contributions made to another state 529 plan.

No. If you are making a withdrawal to cover a qualified education expense for the beneficiary, you are not subject to federal or state income tax.

Qualified education expenses include tuition, certain room and board expenses, fees, books, supplies, computers and equipment required for the enrollment and attendance of the beneficiary at an eligible educational institution, which includes most postsecondary institutions. Review the Plan Description for additional details on eligible expenses and withdrawals.

The earnings portion of a non-qualified withdrawal is subject to federal income taxation, and an additional 10% federal tax. For California taxpayers, the earnings portion of a non-qualified withdrawal may also be subject to California income tax and an additional 2.5% tax. See the Plan Description for details.

The available federal tax benefits for paying qualified education expenses through these programs must be coordinated to avoid the duplication of such benefits. Account owners should consult a qualified tax advisor regarding the interaction under the Internal Revenue Code (IRC) of the federal income tax education-incentive provisions when addressing account withdrawals.

Contributions to a ScholarShare 529 account may help reduce the taxable value of your estate. Learn more about gifting to an existing account. For additional details on tax benefits, we recommend consulting a tax advisor.

There is no federal income tax deduction for 529 plan contributions, regardless of where you live, or which 529 plan you participate in.

Plan contributions are always made after-tax.

At the federal level, rollovers from a 529 plan account to a Roth IRA do not incur federal income tax or penalties.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax.

For California taxpayers, a rollover from a 529 plan account to a Roth IRA will be treated as a non-qualified withdrawal and the earnings portion of the withdrawal will be subject to California state income tax, including the additional 2.5% California tax.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax. Account owners and beneficiaries should consult with a qualified tax professional before rolling over funds from their 529 plan to contribute to a Roth IRA. You are responsible for determining the eligibility of a 529 plan to Roth IRA rollover including tracking and documenting the length of time the 529 plan account has been open and the amount of assets in your 529 plan account eligible to be rolled into a Roth IRA.

Eligible expenses and withdrawals

Qualified higher education expenses include tuition, certain room and board expenses, fees, books, supplies and equipment required for the enrollment and attendance of the beneficiary at an eligible educational institution. This includes most postsecondary institutions. When used primarily by the beneficiary enrolled at an eligible educational institution, computers and related technology such as internet access fees, software or printers are also considered qualified higher education expenses.

Qualified higher education expenses also include certain additional enrollment and attendance costs at eligible educational institutions for any beneficiary with special needs.

Qualified higher education expenses also include (a) qualified expenses in connection with enrollment or attendance at a K-12 primary or secondary public, private or religious school (up to a maximum of $20,000 of distributions per taxable year per beneficiary from all Section 529 programs)1; (b) expenses for fees, books, supplies and equipment required for the participation of a beneficiary in a certified apprenticeship program2; and (c) qualified expenses related to enrollment in a recognized postsecondary credentialing program; and, amounts paid as principal or interest on any qualified education loan of either the beneficiary or a sibling of the beneficiary (up to a lifetime limit of $10,000 per individual).2 (d) make student loan payments. Review the Plan Description for additional information, including the state tax treatment of withdrawals for these expenses.

Footnotes

- 1Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school can be withdrawn free from federal tax. For California taxpayers these withdrawals are subject to state income tax and an additional 2.5% California tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

- 2Withdrawals for registered apprenticeship programs and student loans can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.

Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩

A non-qualified withdrawal is any withdrawal that does not meet the requirements of being a (a) qualified withdrawal; (b) taxable withdrawal; or (c) rollover. The earnings portion of a nonqualified withdrawal is subject to state and federal income taxation and the 10% additional federal penalty tax on earnings (the "Additional Tax"). Non-qualified withdrawals may also be subject to an additional 2.5% California tax on earnings. See the Plan Description for more info.

Your ScholarShare 529 account can be used at eligible colleges, universities, vocational schools, community colleges, graduate or postgraduate programs, apprenticeships, recognized postsecondary credentialing programs and more.1 Contact your school to determine whether it qualifies as an eligible educational institution or use the Federal School Code Search tool on the Free Application for Federal Student Aid (FAFSA) website.

Footnotes

- 1Withdrawals for registered apprenticeship programs can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction, state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.

Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.↩

You may request a withdrawal via your account online. Select the beneficiary you would like to withdraw the money for, click "Make a Withdrawal" on the left-hand navigation and follow the directions. You may also request a withdrawal using the Withdrawal Request Form.

The beneficiary must be enrolled at least half-time at an eligible postsecondary institution. For students living in housing owned and operated by the institution, the full invoice amount will be used to determine the qualified room and board expenses. In the case of students living at home or in off-campus housing, the "cost of attendance" allowance for the individual institution will be used for the qualified room and board expenses.

Computers and related technology such as internet access fees, software or printers are also qualified education expenses. The student must be the primary user of the equipment.

Federal tax treatment of a 529 plan's qualified higher education expenses (QHEEs) includes the repayment of up to $10,000 (including principal and interest) on any qualified education loan of either a 529 plan designated beneficiary or a sibling of the designated beneficiary. To be a qualified expense, the loan repayment amount for an individual is subject to a lifetime limit of $10,000.1 Get additional details in the Plan Description.

Footnotes

- 1Withdrawals for student loan repayment can be withdrawn free from federal and California income tax. If you are not a California taxpayer, these withdrawals may include recapture of tax deduction and state income tax as well as penalties. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

A taxable withdrawal will be subject to applicable state and federal income tax on earnings, if any, but will not be subject to the 10% additional federal tax on earnings (the "Additional Tax").

A taxable withdrawal may also be subject to California income tax but not the additional 2.5% California tax.

Some examples of a taxable withdrawal include a beneficiary's death, permanent disability, receipt of a scholarship award or attendance at a military academy. For more information, review the Plan Description.

Taxable withdrawals that are not subject to the 10% federal penalty tax are withdrawals due to the beneficiary's death, the permanent disability of the beneficiary, the beneficiary's receipt of a scholarship award or certain other tax-free amounts, or the beneficiary's attendance at a military academy. A taxable withdrawal will be subject to applicable state and federal income tax on earnings, if any.

Yes. Funds may be redeposited to your account within 60 days of the refund without penalty should a student need to withdraw from a class. The recontributed amount cannot exceed the amount of the refund.

The SECURE 2.0 Act of 2022, which in addition to a number of significant retirement savings related enhancements, amended Section 529 of the Internal Revenue Code to allow for funds in long-term 529 plan accounts to be rolled over from a 529 plan account to a Roth IRA for the benefit of the 529 account beneficiary.

Account owners may roll money from a 529 account to a Roth IRA for the benefit of the 529 plan account beneficiary without incurring federal income tax or penalties (state tax treatment varies), subject to the following conditions:

- The 529 plan account must be open for 15 or more years, ending with the date of the rollover;

- Contributions and associated earnings that you transfer to the Roth IRA must be in the 529 plan account for more than five (5) years, ending with the date of the rollover;

- The Internal Revenue Code permits a lifetime maximum amount of $35,000 per designated beneficiary to be rolled over from 529 plan accounts to Roth IRAs;

- 529 plan assets can only be rolled over into a Roth IRA maintained for the benefit of the designated beneficiary on the 529 plan account;

- 529 plan assets must be sent directly to the Roth IRA;

- Roth IRA income limitations are waived for 529 plan rollovers to Roth IRAs; and

- The Roth IRA contribution is subject to the Roth IRA contribution limit for the taxable year applicable to the designated beneficiary for all individual retirement plans maintained for the benefit of the designated beneficiary.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax. Account owners and beneficiaries should consult with a qualified tax professional before rolling over funds from their 529 plan to contribute to a Roth IRA. You are responsible for determining the eligibility of a 529 plan to Roth IRA rollover including tracking and documenting the length of time the 529 plan account has been open and the amount of assets in your 529 plan account eligible to be rolled into a Roth IRA.

At the federal level, rollovers from a 529 plan account to a Roth IRA do not incur federal income tax or penalties.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax.

For California taxpayers, a rollover from a 529 plan account to a Roth IRA will be treated as a non-qualified withdrawal and the earnings portion of the withdrawal will be subject to California state income tax, including the additional 2.5% California tax.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax. Account owners and beneficiaries should consult with a qualified tax professional before rolling over funds from their 529 plan to contribute to a Roth IRA. You are responsible for determining the eligibility of a 529 plan to Roth IRA rollover including tracking and documenting the length of time the 529 plan account has been open and the amount of assets in your 529 plan account eligible to be rolled into a Roth IRA.

Beneficiaries

Anyone with a valid Social Security number or taxpayer identification number can be the beneficiary (including the account owner), which is why ScholarShare 529 is a plan for everyone. Learn more about who can open, benefit from and contribute to the ScholarShare 529 plan.

There's no cost associated with opening a ScholarShare 529 account or owning more than one account. You could open a different account for each child.

You might do this to align investment strategies with the time frame each child will begin using the funds. For example, an older child's account could be more conservatively invested to help protect your contributions as they near college, whereas a younger child's account might be invested to balance growth and income strategies during a longer time frame. You may also prefer to pay college expenses first out of your highest growth account to maximize federal tax benefits and to encourage gift contributions from friends and family.

Keep in mind: ScholarShare 529 allows you the flexibility to select multiple investment portfolios within each account. This offers you more control to manage risk on your terms. For example, adding the Guaranteed Portfolio Option can help ensure a portion of your college savings is principal-protected.

Multiple accounts can also aid in estate planning by ensuring that college funds are allocated appropriately to each beneficiary upon the death of the account owner. But if you'd like to stick to one account, you can change any eligible beneficiary at any time and at no additional cost.

Yes. A beneficiary may have more than one ScholarShare 529 account. However, an account owner can have only one account for each beneficiary.

For example, a beneficiary may have an account owned by their parent and/or grandparent and/or aunt, etc. There is an overall maximum account balance limit of $529,000, which applies to all accounts opened for a beneficiary.

Yes. You can change the beneficiary of your account at any time or transfer a portion of your investment to a different eligible beneficiary. The new beneficiary must be an eligible member of the previous beneficiary's family.

For more information, read the form on how to change your beneficiary.

ScholarShare 529 investment options

Here's where you will find performance data for ScholarShare 529's investment options.

ScholarShare 529 offers a variety of smart investment options to fit your life situation, risk tolerance and savings goals. These portfolios vary in investment strategy and degree of risk, allowing you to select a portfolio or combination of portfolios that fit your needs and savings goals.

To compare our ScholarShare 529 investment portfolios, visit our Investment Comparison page. For more information on the investment objectives, risks, charges and expenses, read the Plan Description.

Yes. Each time you make a contribution, you may select from any of the ScholarShare 529 investment portfolio options. Once invested in a particular portfolio, contributions and earnings may be transferred to another investment option twice per calendar year or upon transfer of funds to a plan account for a different eligible beneficiary (see the Plan Description for more information).

To transfer funds between investment portfolios, log in to your account, click "View Details" for your beneficiary, then choose "Change investment options." You may also request and submit by mail the Change of Investment Form.

Contributions and Gifting

A ScholarShare 529 can be started with any amount. How much you need to save will depend on what you plan to use the money for and when.

A few helpful tools:

- Check out the College Savings Calculator to estimate the cost of college.

- Use our College Planning Calculator to see how your savings could add up over time.

You can contribute to a ScholarShare 529 account by any of the following: check, electronic funds transfer, establishing a recurring contribution, establishing payroll direct deposit, rollover from another state's 529 plan account, or redemption proceeds from a Coverdell Education Savings Account or qualified U.S. savings bond. Your contribution will be invested according to your allocation instructions, which you may change at any time online, by telephone or by requesting and submitting the Change of Investment Form.

Contributing to an existing ScholarShare 529 account is easy and secure with our online Ugift® platform. Gift contributions can also be made by check and mailed in. Check with your tax advisor.

For the tax year 2025:

- There's no federal gift tax on contributions you make up to $19,000 per year if you're a single filer or $38,000 if you're a married couple.

- You can also accelerate your gifting with a lump-sum gift of $95,000 if you're a single filer or $190,000 if you're married and prorate the gift over five years per the federal gift tax exclusion.

- You can gift this amount to as many individuals or beneficiaries as you like, free from income tax.

Consult your tax advisor for more details. Learn more about gifting.

To view your transaction history, log in to your account, click "View Details" for your beneficiary and scroll down to the transactions section. You can always speak to one of our college savings specialists at 800-544-5248, Monday through Friday, 8 a.m. to 7 p.m. PT.

There is no maximum ScholarShare 529 contribution limit. However, there is an overall maximum account balance limit of $529,000, which applies to all ScholarShare 529 accounts opened for a beneficiary. Accounts that have reached the maximum account balance limit may continue to accrue earnings.

ScholarShare 529 accounts can be opened with any amount, and contributions of any amount can be made. Check out our unique gifting feature to see how you can easily and securely ask for and manage gift contributions to your ScholarShare 529.

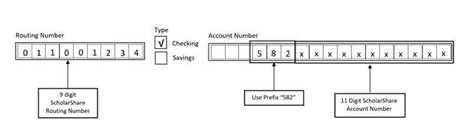

Have the Franchise Tax Board deposit some or all of your refund directly into one or more of your ScholarShare 529 College Savings Plan accounts.

- Complete the Refund or No Amount Due section, line 115, of CA Form 540 to authorize Direct Deposit (line 32 of CA Form 540 2EZ)

- Provide the ScholarShare 529 routing number (011001234)

- Select Checking for Type

- For Account Number use a prefix of 582 + your 11 digit ScholarShare account number. DO NOT use leading or trailing zeroes.

- See summary here:

Financial aid and scholarships

Assets in a parent-owned 529 account have less of an impact on financial aid than some other savings methods. Expected Family Contribution (EFC) calculations for financial aid generally factor parent assets outside of retirement savings at approximately 5%, whereas student assets are generally factored in at 20% or more. Therefore, a parent-owned 529 account may have less of an impact on financial aid eligibility than assets owned by the student.1

Footnotes

- 1The treatment of investments in a 529 savings plan varies by school. Assets are typically treated as the account holder's and not the student's. (Student assets are generally assessed at 20%, whereas parental assets are generally assessed at 5.6%.) Any investments, including those in 529 accounts, may affect the student's eligibility to get financial aid based on need. You should check with the schools you are considering regarding this issue.↩

If the beneficiary receives a scholarship that covers the cost of qualified expenses, you can withdraw the funds from your account up to the amount of the scholarship without incurring the 10% federal tax penalty on the earnings portion. However, the earnings portion will be subject to federal and state income tax. If the amount withdrawn exceeds the amount of the scholarship, the earnings portion of the amount withdrawn will be subject to the additional 10% federal penalty tax and an additional 2.5% California tax on earnings. Please consult with a qualified tax advisor or consultant.

Historically, withdrawals from grandparent–owned 529 plans have been considered untaxed income to the student and added to the student's adjusted gross income on the FAFSA. Beginning with the 2024-2025 FAFSA, withdrawals from grandparent–owned 529 plans will no longer need to be reported on the FAFSA or negatively affect the student's eligibility for federal financial aid. FAFSA simplification is subject to change. You should check with the schools you are considering regarding this issue. For assistance or help completing FAFSA click here.

Opening an account

Anyone with a valid Social Security number or taxpayer identification number can open a ScholarShare 529 account. Accounts can be opened online or by downloading enrollment materials.

You can also open an account by requesting a mailed enrollment kit online or by giving us a call at 800-544-5248.

There are no sales charges, startup or maintenance fees associated with ScholarShare 529 accounts. For details on total annual asset-based fees, comprised of the underlying investment expenses for each investment option, the plan manager fee and state administration fee, review the Plan Fees for each individual investment portfolio.

Yes. Whether you have recently moved to the state, have an underperforming or higher-cost 529 plan, or just want to simplify, consolidating 529 accounts into ScholarShare 529 is easy. You can transfer funds from another 529 plan to your ScholarShare 529 account for the same beneficiary once within a 12-month period without incurring tax penalties.

Consolidating education savings into ScholarShare 529 also gives you a single view of your savings and performance as well as single-step payments to colleges, universities, K-12 schools, etc.1

You may also save money that can go right back into your college fund. ScholarShare 529 expenses are less than half the national average for 529 plans.2 You pay no sales charges, start up or maintenance fees.

The 529 plan from which you are transferring funds may be subject to different features, costs and surrender charges. As such, you should consult your tax advisor or the other 529 college savings plan prior to making any decisions. For more information, see How to manage an incoming rollover from another 529 saving plan account.

Footnotes

- 1Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school can be withdrawn free from federal tax. For California taxpayers these withdrawals are subject to state income tax and an additional 2.5% California tax. You should talk to a qualified professional about how tax provisions affect your circumstances. K-12 withdrawals are limited to $20,000 per year for K-12 tuition.↩

- 2Source: ISS Market Intelligence 529 College Savings Fee Analysis Q4 2025. ScholarShare 529's average annual asset-based fees are 0.21% for all portfolios compared to 0.49% for all 529 plans.↩

Log in to sign up for electronic delivery for statements, transactions, profile confirmations and tax forms.

Learn more about Two-Factor Authentication and Aggregators.

What's next?

-

Explore our plan

Learn more about eligibility and all the qualifying expenses a ScholarShare 529 can cover.

How our 529 works -

Compare investment options

We make it easy to choose investment options that fit your financial needs and savings goals.

Discover your options -

Ready to get started?

Open an Account